Login

Login

Canadian inflation data for August broadly matched expectations, seeing annual all-items price growth of 1.9% YoY, and keeping the BoC on track to cut rates tomorrow. Underlying price pressures remain elevated, but showed no signs of strengthening further, meaning that labour market weakness should continue to be the primary focus for policymakers.

From a USDCAD perspective, attention now turns to the Governor Macklem for any forward guidance on Canadian rates, and to the FOMC, who are also set to deliver its own rate decision on Wednesday afternoon. The latter, we suspect, will be more consequential for loonie fortunes, given our expectations for a non-committal stance on further easing from the Governing Council.

Admittedly, our expectation for a lack of concrete BoC guidance stems more from the Governing Council’s prior tendencies than from the content of this latest data release. If anything, today’s data landed a little softer than expected, with prices falling -0.1% in August, against consensus expectations for all-items CPI to remain unchanged.

This was also enough to see annual inflation undershoot economist forecasts by 0.1pp, though base effects ensured that this still produced a 0.2pp rise over July’s 1.7% YoY price growth rate. Still, with the data proving marginally more dovish than consensus forecasts, that would favour marginally more dovishness from the BoC, all else being equal.

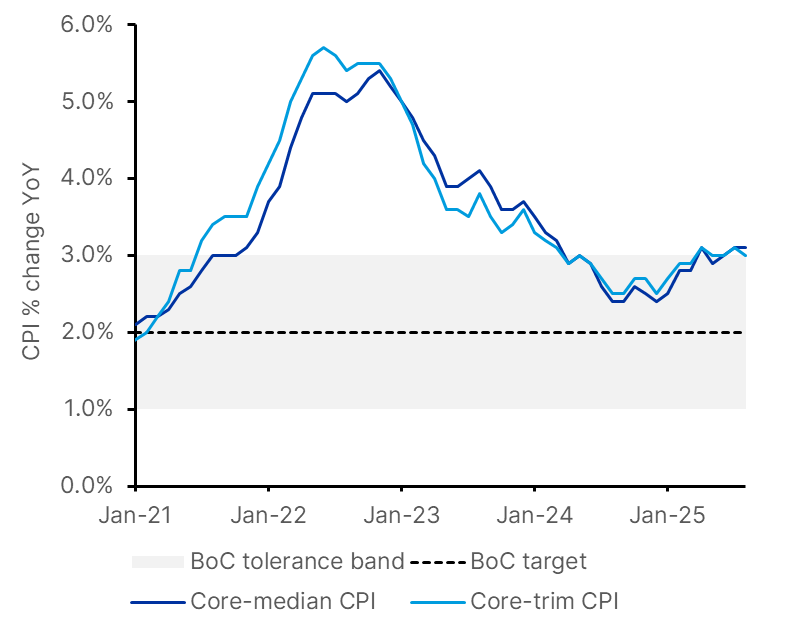

This is doubly true when considering recent labour market prints, with the economy shedding 65.5k jobs in August, after losing 40.8k in July. The unemployment rate now stands at 7.1%, a level last seen in mid-2026, pandemic-era excluded. Yet despite this, annual core-median and core-trim price growth again printed at the top of the BoC’s tolerance band, and continues to look somewhat sticky. The former remained unchanged at 3.1%. The latter dropped 0.1pp from a July reading that was revised up by the same amount, ultimately leaving this measure at 3.0% YoY, unchanged from initial estimates.

Putting this together, we think labour market weakness should give the BoC some confidence that price growth will cool moving forward, but the lack of recent movement in underlying measures weighs against pre-committing to additional rate cuts beyond this week’s decision.

Similarly, this is a point reinforced by some of the details of the August CPI report. On the one hand, shelter inflation – a significant component propping up headline price growth in recent years – slipped to just 2.6% YoY in the August data. This is down from 3.0% previously, and the slowest rate of annual growth since March 2021. But adjusting for housing costs, core CPI ex-shelter is now running at 1.9% YoY, up from 1.7% in July. The broader all-items CPI, excluding rent and mortgage costs, rose from 1.2% to 1.5% in this latest set of figures. We are inclined to see this as healthy normalisation, rather than any cause for immediate concern. Nevertheless, such a broadening in price pressures warrants a degree of caution from the Governing Council.

All told then, we see this latest CPI report as nicely confirming our priors. It contains few, if any, reasons not to cut rates by 25bps on Wednesday, but enough to weigh against pre-committing to a follow-up move in October. Granted, we still expect at least one further dose of easing to be delivered before year-end in light of the current economic slowdown.

But more immediately, a non-committal stance from the Governing Council should prevent markets from pricing this in right away, supporting loonie upside against the greenback, assuming the Fed also matches our expectations and kicks off a more sustained easing cycle with their own rate decision later tomorrow afternoon.

Underlying price growth proved little changed in August, enough to ensure a BoC rate cut this month, but sufficiently sticky that the Governing Council is unlikely to pre-commit to a follow up move

Author:

Nick Rees, Head of Macro Research